How do I qualify for a USDA loan in Florida

By Andrew Henderson

NO down payment – Finance 100% of your home.NO maximum USDA loan amount in Florida.NO assets needed to qualify.Flexible credit guidelines.Competitive, fixed interest rates so payments do not increase.USDA Loans are for new and existing properties.

What are the cons of a USDA loan?

- Only primary residences can be purchased. USDA loans cannot be used to purchase a vacation home or rental property.

- There are geographical restrictions. Homes in urban centers won’t qualify. …

- There are income limits. …

- Mortgage insurance is factored into the cost.

What's the difference between a USDA loan and a regular loan?

Conventional loans are available nationwide. USDA loans, on the other hand, are only available in eligible rural areas as determined by the USDA. If you’re located in a major metropolitan area, you likely won’t be able to get a USDA loan.

What is the income limit for USDA loan in Florida?

USDA eligibility for a 1–4 member household requires annual household income to not exceed $91,900 in most areas of the country, and annual household income for a 5–8 member household to not exceed $121,300 for most areas.Is it hard to get a USDA loan?

The USDA home loan is available to borrowers who meet income and credit eligibility requirements. Qualification is easier than for many other loan types, since the loan doesn’t require a down payment or a high credit score.

Who pays closing costs on USDA loan?

USDA Closing Costs Paid By Seller Rather than bringing more cash to close, USDA loans allow the seller to pay up to 6% of the sales price towards the buyer’s closing costs. Therefore, the seller may pay part or all of the buyer’s closing costs.

Why would USDA deny a loan?

Things like unverifiable income, undisclosed debt, or even just having too much household income for your area can cause a loan to be denied. Talk with a USDA loan specialist to get a clear sense of your income and debt situation and what might be possible.

What is the USDA income limit?

USDA Loan Income Limits and Eligibility in 2021 The current standard USDA loan income limit for 1-4 member households is $91,900, up from $90,300 in 2020. The 2021 limit for 5-8 member households is $121,300, up from $119,200. USDA loan limits by county may be higher to account for cost of living.Is a USDA loan a good idea?

Is a USDA loan good? A USDA loan is a great option for buyers with moderate or low income. It lets you buy a house with nothing down and low mortgage rates – two huge benefits that only one other loan program (the VA loan) offers. If your home is in an eligible area, it’s worth exploring a USDA–guaranteed loan.

What is the minimum credit score for a USDA loan?The USDA doesn’t have a fixed credit score requirement, but most lenders offering USDA-guaranteed mortgages require a score of at least 640, and 640 is the minimum credit score you’ll need to qualify for automatic approval through the USDA’s automated loan underwriting system.

Article first time published onHow long does it take for a USDA loan to be approved?

Borrowers can typically expect the USDA loan process to take anywhere from 30 to 60 days, depending on the qualifying conditions. Check your USDA loan eligibility here.

Do sellers like USDA loans?

Sellers should have no concerns about accepting a USDA buyer’s offer. Like many things in regards to mortgages, a lot comes down to the lender and their ability to communicate and close loans efficiently.

Is a USDA loan better than a bank loan?

This program helps low- to moderate-income households buy safe and comfortable dwellings in designated rural areas. These houses may be sited on acreage that disqualifies them for other types of financing. For many, USDA loans are a better option than traditional financing.

Can I get a USDA loan with a 580 credit score?

The minimum credit score requirement for a USDA loan is now a 640 (for an automated approval). Fortunately, you can still get approved for a USDA loan with a 580 credit score, but it will require a manual approval by an underwriter. … Other requirements for USDA loans are that you purchase a property in an eligible area.

Can you buy land with a USDA loan?

A USDA construction loan can finance the land, build your home, and serve as your long–term mortgage – essentially rolling three loans into one. Plus, there’s no down payment required and only one set of closing costs. However, these loans can be hard to find.

Does USDA require down payment?

USDA loans require no down payment, unlike FHA and conventional loans. The USDA monthly guarantee fee is lower than FHA monthly mortgage insurance in most cases, and you may be able to roll these fees into your loan.

Does USDA pull your credit?

As we mentioned earlier, the USDA loan is very forgiving when it comes to credit scores. This program allows as low as a 620 mortgage credit score. That’s pretty aggressive for a no-money-down purchase! Typically, a 620 credit score means using the middle of 3 credit scores pulled by the lender.

What happens when your loan goes to USDA?

Once the lender/bank is finished, they approve the file and forward to the USDA Rural Housing office for the final approval or “final commitment” as it’s known. Once the USDA office has the file, they generally take up to a week to issue the final commitment and send it back to the bank or lender for closing.

Can I get a USDA loan with collections on my credit?

USDA Loan Requirements Although it is possible to qualify for a USDA loan with collections on your credit report, USDA guidelines state that you must make payment arrangements with the collection agency before it will guarantee your loan.

Can closing costs be rolled into a USDA loan?

Typically, you can’t pay for your closing costs using your loan (also referred to as rolling in your closing costs). However, USDA loans allow borrowers to roll some or all of their closing costs into their mortgages if the home appraises for more than the sales price.

Can closing costs be rolled into the loan?

Most lenders will allow you to roll closing costs into your mortgage when refinancing. Generally, it isn’t a question of which lender that may allow you to roll closing costs into the mortgage. It’s more so about the type of loan you’re getting – purchase or refinance.

Are USDA loans hard to close?

With an FHA, VA, or conventional loan, the lender can completely approve and close the loan on its own. USDA, however, requires a hands–on check by USDA staff. The process can take an extra few days or up to three weeks or more depending on the backlog at your state’s USDA office.

Is USDA for first time home buyers?

Also, USDA loans are available to both first-time and repeat home buyers. Even though the loan comes with low mortgage rates, no down payment, and low insurance costs, fewer than 5% of mortgages are USDA loans.

What's the difference between FHA and USDA loans?

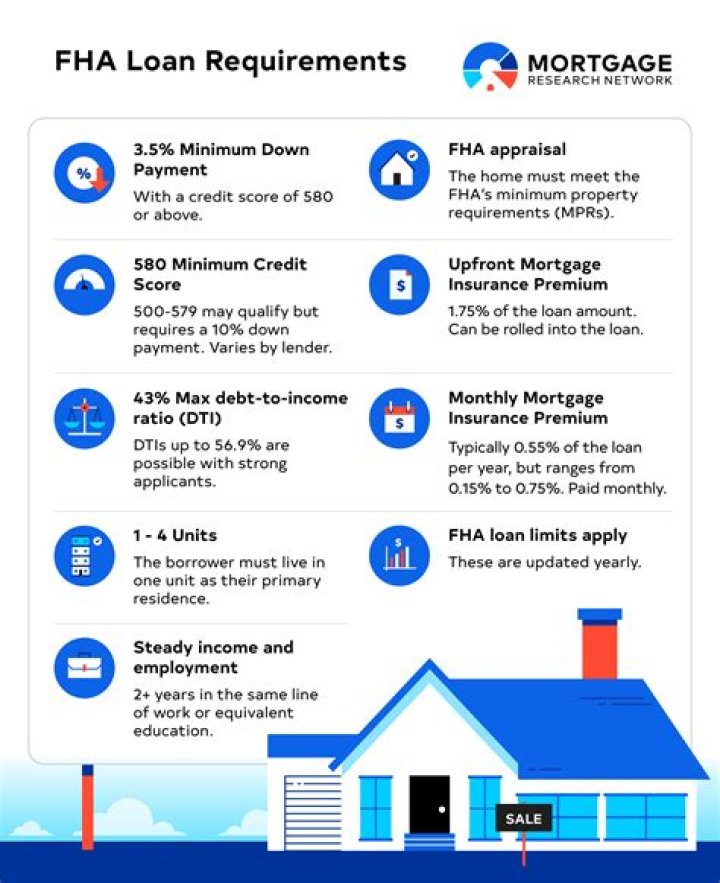

USDA loans offer 100 percent financing, meaning there is no down payment required. FHA loans, on the other hand, require at least 3.5 percent down. Though this is less than conventional loans often require, it does mean the buyer must put down a lump sum of cash up front.

Is USDA funded for 2021?

2021 FUNDING OVERVIEW Funding for mandatory programs is estimated to be $128 billion, $3 billion more than 2020 enacted levels. Including negative receipts, offsetting collections, recoveries, etc., USDA is requesting a total of $146 billion in 2021 available funds.

Does USDA have a maximum loan amount?

The USDA does not set loan limits as with FHA loans, but bases the maximum loan amount on the borrower’s ability to qualify. As mentioned above, there is no maximum loan limit with the USDA Guaranteed Loan.

Can I sell my house if I have a USDA loan?

Answer: Yes, assuming you have a standard USDA 502 Guaranteed loan (no special subsidy) You can sell your house and pocket the profits just like any other home sale. You can also use the USDA home loan again (on your next home) if you still meet the eligibility and qualifying requirements.

Does USDA have a 90 day flip rule?

Appraisal Updates • An appraisal report is initially valid for 150 days from the effective date • Lenders may extend that period to 240 days (an extra 90 days beyond the initial period) with a one-time Appraisal Update Report. Property flipping is not prohibited. appraiser.

How can I get out of a USDA loan?

There are no options to remove or avoid the USDA annual fee unless the mortgage is refinanced to another product or the mortgage is paid off. Learn more about USDA household income limits or property eligibility.