Do you have to pay escrow upfront

By Michael Gray

You will have to prepay some of your escrow costs at closing. For example, your lender might make you pay upfront for your first year of homeowners insurance. … Your lender might require, for instance, 3 months of property tax payments upfront to establish your escrow account.

Is escrow paid in arrears?

The property tax portion is placed in an escrow account and is used to pay your property tax bill when it comes due. … Therefore, your lender is also paying from your account in arrears even though you don’t see this payment being made.

What is the initial escrow payment at closing?

An initial escrow deposit is the amount that you will pay at closing to start your escrow account, if required by your lender. This initial amount may be different from what you pay monthly to maintain the escrow account. This initial amount is listed in section G on page 2 of your Loan Estimate.

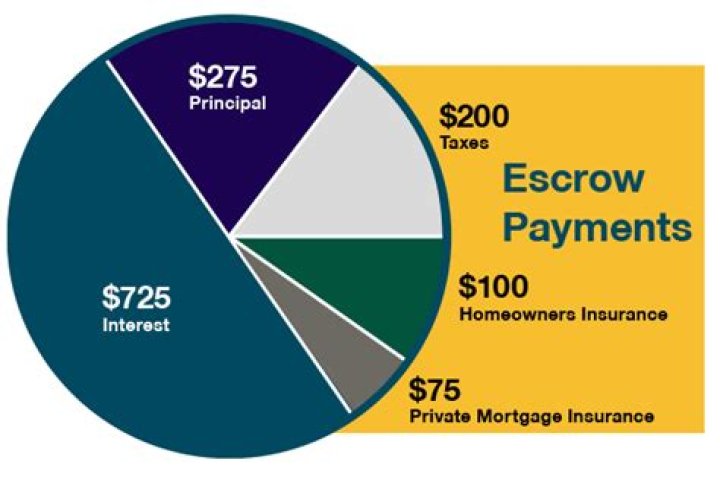

How does escrow payment work?

Each month, the lender deposits the escrow portion of your mortgage payment into the account and pays your insurance premiums and real estate taxes when they are due. Your lender may require an “escrow cushion,” as allowed by state law, to cover unanticipated costs, such as a tax increase.How long do you pay escrow?

When you’re in the process of buying a home, you’re “in escrow” between the time that your offer — with its cash deposit — is accepted and the day that you close and take ownership. That’s usually at least 30 days.

Is escrow included in mortgage payment?

The good news is that most lenders require you to set up an escrow account under the terms of your mortgage that fold in most of these costs for you. This means that your monthly mortgage payment will also include an escrow payment to cover your property taxes and insurance premiums.

Why is my escrow balance so high?

The most common reason for a significant increase in a required payment into an escrow account is due to property taxes increasing or a miscalculation when you first got your mortgage. Property taxes go up (rarely down, but sometimes) and as property taxes go up, so will your required payment into your escrow account.

What happens if I pay an extra $200 a month on my mortgage?

Since extra principal payments reduce your principal balance little-by-little, you end up owing less interest on the loan. … If you’re able to make $200 in extra principal payments each month, you could shorten your mortgage term by eight years and save over $43,000 in interest.What does escrow disbursements made on your behalf mean?

An escrow disbursement is a payment out of an escrow account, usually by the lender on behalf of a borrower to cover property taxes and homeowners insurance.

Can you lose money in escrow?You pay escrow to seal the deal after a property owner accepts your offer. While these funds show the seller you’re serious about purchasing the dwelling, if you can’t close the loan, you could lose your escrow money. However, everything depends on your sales contract and the contingencies included.

Article first time published onIs escrow good or bad?

Escrows are not all bad. There are good reasons to maintain an escrow: … The lender benefits by having an escrow in place for taxes and insurance because it protects them against the risk of the collateral for their loan (your home) being auctioned off by the county if those expenses are not paid.

What happens after closing escrow?

The earnest money is released from the escrow account and the lender cuts the seller a single big check. Unless the buyer and seller have otherwise negotiated, the buyer takes official possession of the property on the actual date of closing.

Is PMI included in escrow?

Lenders use PMI to protect their losses should you default on the house. Your PMI payment is paid into an escrow account and issued to the appropriate creditor by your lender when it’s due.

Is it better to pay extra on principal or escrow on a mortgage?

If you’re stuck between paying down the balance on the principal or escrow on your mortgage, always go with the principal first. By paying towards the principal on your mortgage, you’re actually paying on the existing debt, which brings you closer to owning your home.

Is an escrow advance bad?

If your escrow account’s balance is negative at the time of the escrow analysis, the lender may have used its own funds to cover your property tax or insurance payments. In such cases, the account has a deficiency. … If the amount exceeds one month’s escrow payment, the lender may give you two to 12 months to repay it.

What is escrow advance?

An escrow advance represents the additional funds paid on behalf of the borrower by the servicer when there are insufficient funds in the escrow account to satisfy the entire payment of an escrow account item that has come due.

Why did my mortgage go up $100?

You have an escrow account to pay for property taxes or homeowners insurance premiums, and your property taxes or homeowners insurance premiums went up. … If your monthly mortgage payment includes the amount you have to pay into your escrow account, then your payment will also go up if your taxes or premiums go up.

Do I get my escrow money back when I refinance?

When you refinance a loan, the original escrow account remains with the old loan. … All the property tax and insurance payments you have made to that account, since the last payment was made, will be returned to you, usually within 45 days via wire transfer or check.

How can I remove escrow from my mortgage?

You must make a written request to your lender or loan servicer to remove an escrow account. Request that your lender send you the form or ask them where to obtain it online, such as the company’s website. The form may be known as an escrow waiver, cancellation or removal request.

Why did I get a escrow refund check?

Typically, when you take out a mortgage, your lender requires you escrow your taxes and insurance. This means that you pay money toward these annual expenses when you make your monthly principal and interest payments. … If your escrow account contains excess funds, then you receive an escrow refund check.

How can I pay off my 30 year mortgage in 15 years?

- Adding a set amount each month to the payment.

- Making one extra monthly payment each year.

- Changing the loan from 30 years to 15 years.

- Making the loan a bi-weekly loan, meaning payments are made every two weeks instead of monthly.

How can I pay my house off in 10 years?

- Purchase a home you can afford. …

- Understand and utilize mortgage points. …

- Crunch the numbers. …

- Pay down your other debts. …

- Pay extra. …

- Make biweekly payments. …

- Be frugal. …

- Hit the principal early.

Can I pay off my mortgage in 5 years?

A 15-year loan term may feel like a far cry from your five-year payment plan but if there are no prepayment penalties, you can still pay it off in five years and benefit from the lower interest rate along the way.

How can I avoid losing my escrow deposit?

- Ask for contingencies. You can request that your earnest money deposit be contingent on your getting financing or the house passing inspection. …

- Be 100 percent sure before you offer. …

- Use a trusted real estate agent.

Why is escrow bad?

There are some advantages to going without an escrow service – your money can earn you interest and you may be eligible for early payment discounts for some bills. But, the disadvantages are obvious – you are required to pay your tax bills and insurance payments on time or risk losing your house.

How do escrow companies get paid?

There is no industry standard, though the simplest solution is to split escrow fees between the buyer and seller. Otherwise, negotiations can lead to escrow services being paid entirely by the buyer or paid by the seller as seller concessions.

Is the house yours after closing?

After you finish signing at the closing of your new house, you’re handed the keys and the house is officially yours.

Can a lender back out after closing?

The lender has no right of rescission. Once you have signed loan documents, you have entered into a binding contract, and the lender is legally bound to honor those signed documents. The right of rescission is a separate form giving you three days in which you can back out of the transaction without penalty.

What should you not do in escrow?

- Watch those zero-balance credit cards. …

- Don’t change jobs – or let your lender know if you do. …

- Don’t buy or lease a new car. …

- Don’t buy new furniture on store credit. …

- Don’t run up credit cards with cash advances:

What is the 28 rule in mortgages?

One way to decide how much of your income should go toward your mortgage is to use the 28/36 rule. According to this rule, your mortgage payment shouldn’t be more than 28% of your monthly pre-tax income and 36% of your total debt. This is also known as the debt-to-income (DTI) ratio.